BUYER RESOURCE CENTER

Buying Your DVC Membership

Expert guides and resources to help you buy Disney Vacation Club with confidence.

111

Articles

5-Star Rated

2026

Updated

Best DVC Resale Broker

How to Buy DVC Points

How do I tell if a DVC listing is fairly priced?

DVC Resale Sites

Best DVC Resale Sites

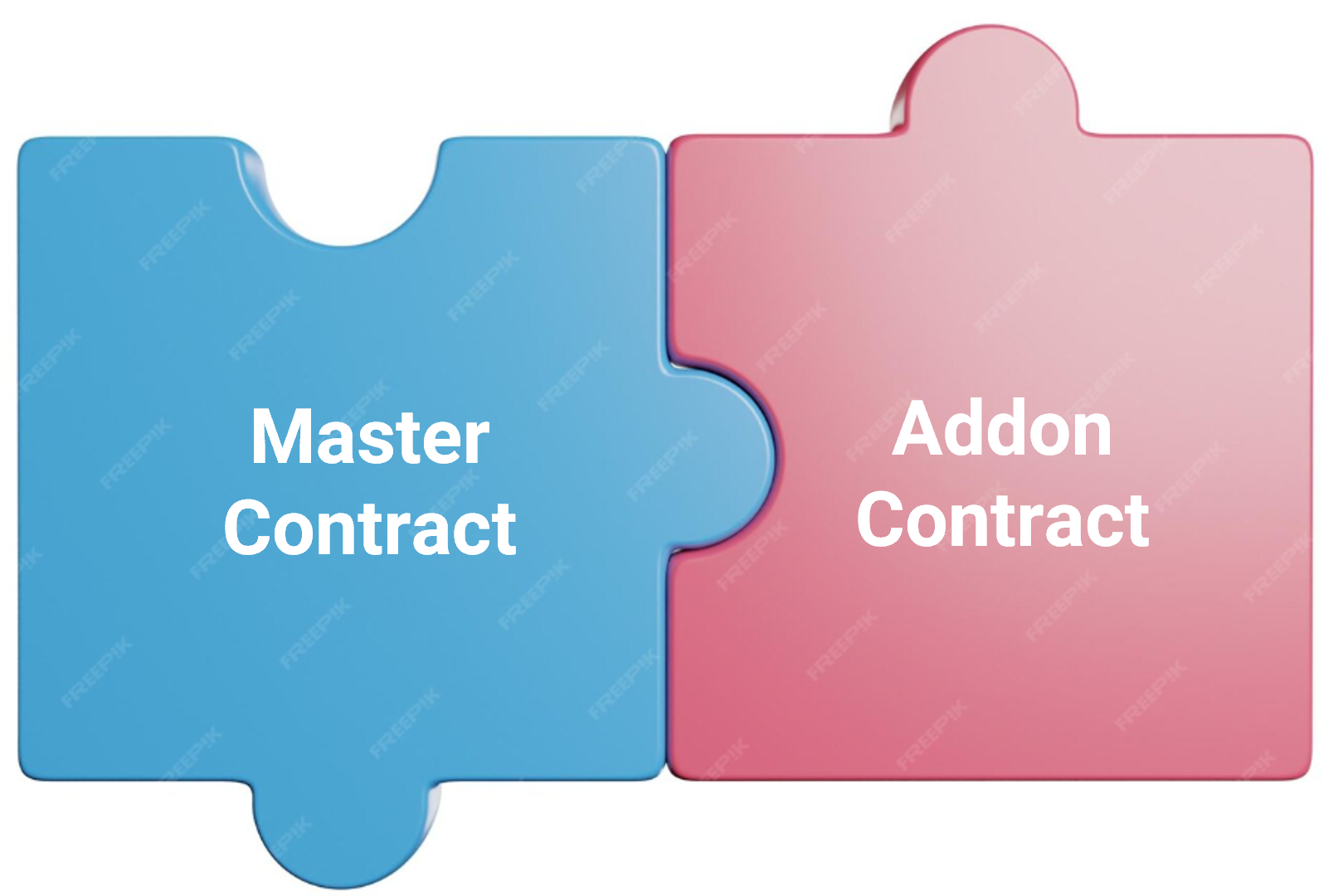

Understanding DVC Resale contract Restrictions

Best DVC Resale Site Renamed

How DVC Sales Works

DVC Resale Process

Linking a DVC Resale Purchase to Your Disney Account

Closing Timeline Guide

DVC Resale: Seller Banking Requests

Adding my Disney DVC to a trust?

Add Resale Contract to DVC Account

Understanding Disney DVC Resale History

DVC Resale Points

Disney Resale DVC

DVC Points Resale

Can You Buy DVC Resale from Disney?

Resale Restrictions

Buying DVC Resale from Disney

Buying DVC Resale Direct from Disney

Buying Resale DVC Points

Buy DVC Timeshare Resales

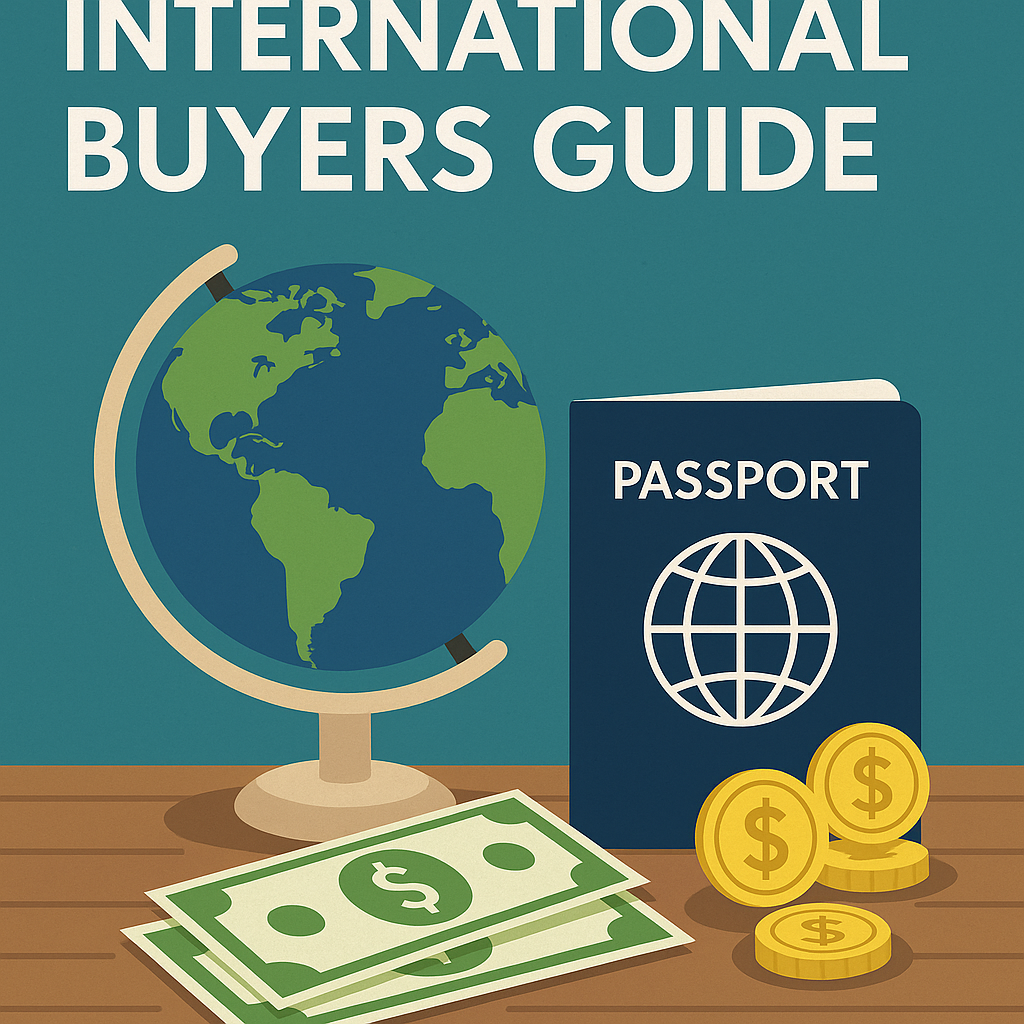

International Buyers Guide

Buy DVC Resale Points

Buy DVC Resale Contract

Buy DVC Points Resale

Buying DVC Points Resale

Buy DVC Resale

DVC Resales Listings | Buy DVC Contracts

Buying DVC Resale

Why Use DVC Sales

Best Place to Buy DVC Resale

Best DVC Resale Company

DVC Buy Resale

DVC Resale Listings

Disney DVC Resale Search Engine

DVC Resale Listings Search Engine

DVC Resale Search Engine

DVC Resale Aggregator

Disboards DVC Resale

Disadvantages of Buying DVC Resale

Cons of Buying DVC Resale

Resales DVC

DVC Resale

DVC Point Resale

DVC for Resale

DVC Timeshare Resale

Resale DVC Points

DVC by Resale

DVC Contract Resale

DVC Resale Contracts

Buying DVC Resale Pros and Cons

Buying DVC Direct vs Resale

Buying DVC from Disney or Resale

DVC Resale Value

DVC Resale vs Direct

DVC Direct vs Resale

DVC Resales Value

DVC Resale vs Direct

DVC Resale Market

DVC Resale Limitations

Disney DVC Resale Restrictions

DVC Resale Restrictions

Best DVC Resort to Buy Resale

Best DVC Resale

Cheapest DVC Resale

Average DVC Resale Prices 2025

Average DVC Resale Prices

DVC Resale Prices

Where Can I Use DVC Resale Points

Buy DVC Points: What You Need to Know Page title

Disney Vacation Club

disney vacation club point chart

DVC Resort Expiration

DVC Resale vs. Retail

Buying DVC Resale vs Direct

DVC Points For Sale

DVC Resale Market Listings

DVC Resale Brokers

DVC Resales

Disney Vacation Club Resale Listings

dvc membership resale

How to buy DVC resale

Should I buy DVC from Disney or Resale

DVC Resale Animal Kingdom

Disney DVC Resale Market

where to buy dvc resale

dvc resale annual pass discount

DVC Resale Store

DVC Resale Companies

Disney DVC Points for Sale

Disney Vacation Club for Sale

DVC Resale Companies

Buy Disney Vacation Club Points

DVC Resale Vero Beach Resort

DVC Resale Saratoga Springs

DVC Resale Boulder Ridge

DVC Resale Riviera Resort

DVC Resale Grand Californian

DVC Resale Fort Wilderness

DVC Resale Disneyland Hotel

DVC Resale Copper Creek

DVC Resale Boulder Ridge

DVC Resale BoardWalk

DVC Resale Beach Club

DVC Resale Bay Lake Tower

DVC Resale Aulani

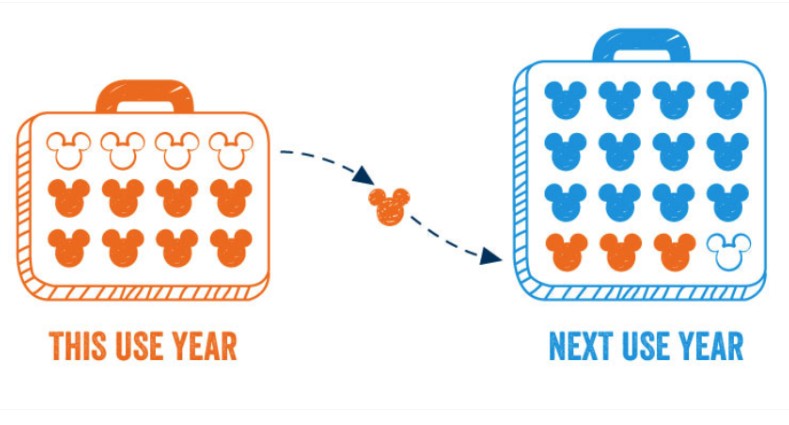

Banking and Borrowing DVC Points

Home Resort Priority

No matching articles

Try different keywords

Can't Find What You Need?

Our support team is ready to help with any questions.